Building an accessory dwelling unit in San Diego requires thoughtful financing strategies that combine construction loans, home equity lines, and municipal programs. With construction costs rising and new loan programs emerging, San Diego homeowners need clarity on the ADU financing options that are available in 2026.

From San Diego ADU design and permits to securing the right loan amount, this guide by Streamline Design & Permitting explains how to finance your ADU project while minimizing borrowing costs and maximizing rental income potential.

The Current State of ADU Policy in San Diego

San Diego's ADU landscape evolved significantly in 2025, creating a refined framework for 2026 that impacts how lenders evaluate loan programs. New ADU rules rolled out in 2025 aim to balance housing needs with neighborhood compatibility. The city tightened density bonus eligibility in lowest-density zones and added fire-safety restrictions in hillside areas, while a new Community Enhancement Fee now applies to bonus units under 750 square feet.

Despite these restrictions, the City of San Diego maintains streamlined permitting for compliant projects, with expanded pre-approved plans providing predictable routes to construction that reduce soft costs and improve your ability to secure financing from reputable lenders.

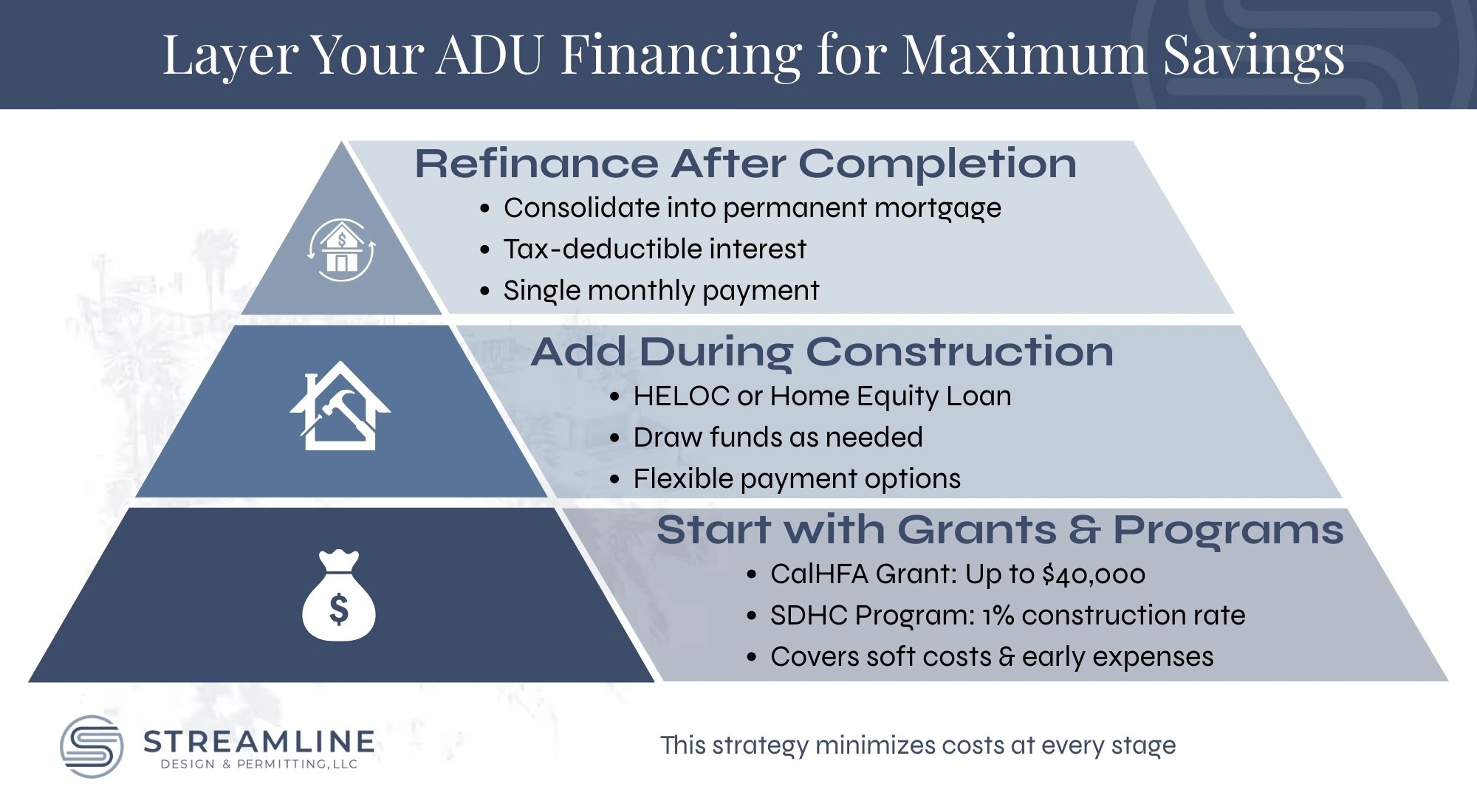

How San Diego ADU Financing Works

Most San Diego homeowners combine multiple financing options to fund ADU construction, layering a home equity line of credit with construction financing before refinancing into a permanent mortgage after completion. The ideal approach for you depends on your existing equity in your primary residence, your ability to generate rental income, and whether you qualify for programs like the San Diego ADU Bonus Program.

Key factors affecting your financing strategy:

- Available equity in your current loan or existing mortgage.

- Projected future appraised value and post-construction value.

- Your ability to carry interest-only payments during the construction phase.

- Whether you qualify for affordable housing programs with income verification.

The right combination minimizes interest rates and closing costs while maximizing your cash-out opportunity from significant equity in your home.

Comparing San Diego ADU Financing Options

In 2026, private lending matured, with financial institutions treating ADUs as standard property improvements through renovation loans, home equity loans, and cash-out refinance products. San Diego homeowners with equity can choose from several ADU financing options without replacing low-interest first mortgages.

San Diego SDHC ADU Finance Program

The San Diego Housing Commission's ADU Finance Program offers the most aggressive municipal financing available in 2026. This construction-to-permanent loan provides up to $250,000 at 1% interest during the construction phase, converting to 4% fixed for 15 years after completion.

Program benefits for San Diego ADU construction:

- Nominal 1% rate during construction reduces interest-only payments.

- No requirement for significant equity in the present loan amount.

- Includes pre-reviewed construction drawing templates worth $10,000-$25,000.

- Makes ADU projects possible for homeowners who can't secure traditional ADU loans in San Diego.

The program requires a seven-year affordability covenant that restricts tenants to households earning 80% or less of the Area Median Income. As a result, this creates naturally occurring affordable housing while providing extremely low borrowing costs that help you generate rental income immediately.

Home Equity Line of Credit (HELOC)

A home equity line continues to be one of the most flexible financing options for ADU projects. This allows you to borrow against your home's equity and withdraw funds as needed during construction while paying interest only on what you use.

Credit unions like San Diego County Credit Union and Mission Federal Credit Union offer competitive variable rates expected to decline through 2026, making HELOCs ideal for phased construction with minimal closing costs. Combined loan-to-value rules limit total borrowing, typically capped at 80-90% CLTV.

After-Repair Value Renovation Loans

Specialized renovation loans from reputable lenders base loan amounts on post-construction value rather than current equity, unlocking $100,000-$200,000 in additional capacity compared to standard home equity loans.

These loan programs require firm construction contracts and detailed design and contractor bids that demonstrate the completed unit’s income-generating capacity. The loan offer should outline terms that typically carry rates 1-2 percentage points higher than conforming mortgages.

Cash-Out Refinance Strategy

The Federal Housing Finance Agency increased conforming loan limits for San Diego County to $1,104,000 for one-unit properties in 2026. In return, this created significant cash-out refinance opportunities for homeowners who can stay within conforming limits while accessing construction capital.

When you refinance an existing mortgage and extract cash for ADU construction, you stay within conforming limits and avoid stricter jumbo loan requirements, though this strategy works best when current interest rates are comparable to your existing mortgage rate.

CalHFA ADU Grant Program and Fee Waivers

The CalHFA ADU Grant Program historically provided up to $40,000 for pre-development expenses, including technical drawings, permitting costs, structural engineering, and site surveys. While the initial allocation was fully committed, homeowners should monitor the California Housing Finance Agency website for supplemental appropriations that could reduce their loan amount by covering soft costs.

Senate Bill 13 mandates development impact fee waivers for ADUs under 750 square feet in 2026, saving approximately $20,000 in traffic impact fees and utility capacity charges. Junior ADUs under 500 square feet are exempt from school fees, while SB 543 clarifies that the threshold applies only to the interior livable space. California's Department of Housing and Community Development provides comprehensive guidance on qualifying for these reductions.

Reverse Mortgage Options for Seniors

Homeowners aged 62 and older with significant equity can access funds through a Home Equity Conversion Mortgage (HECM loan) that the Federal Housing Administration backs. These recourse FHA loans don't require a minimum monthly payment during the homeowner's lifetime, allowing the owner to take equity from their primary residence without traditional debt payments.

The HECM loan becomes due when the homeowner sells, moves permanently, or passes away, making this financing strategy particularly effective for multigenerational housing projects. Required third-party financial counseling through a financial advisor ensures homeowners understand the long-term implications before securing financing.

Smart Financing Strategies and Tax Implications

The most effective ADU financing San Diego strategy layers multiple sources rather than relying on a single loan. Start with CalHFA grants or SDHC programs for soft costs, add HELOCs or home equity loans during the construction phase, then refinance into a permanent mortgage that consolidates debt with tax-deductible interest costs.

Federal tax credits and local incentives include:

- Section 45L provides $2,500-$5,000 for ENERGY STAR-certified ADUs before July 2026.

- Third-party solar leases satisfy Title 24 requirements with zero upfront capital.

- Vista, La Mesa, and Encinitas offer additional fee waivers beyond state requirements.

- ENERGY STAR 45L program lists certification requirements.

San Diego County Assessor uses a blended assessment approach where your original primary residence maintains its Proposition 13 protected base year value, while only new construction gets added to the tax roll. At San Diego's effective 1.2% tax rate, a $150,000 ADU increases annual property taxes by approximately $1,800.

Proposition 19 creates reassessment risks for inheritance transfers unless the heir moves in as their primary residence within one year. Review California's property tax guidelines before planning multigenerational transfers to avoid unexpected reassessment.

Costs & Realistic Budgets for San Diego ADUs

Costs and budgets are one of the most integral factors in whether a project moves forward as planned. Construction costs for San Diego ADUs in 2026 range from $120,000-$180,000 for garage conversions to $250,000-$400,000 for detached units.

At Streamline Design & Permitting, we create construction plans that lead to accurate bids from contractors. This solid planning prevents costly surprises that drain your construction loan during the building phase.

Risk mitigation strategies for securing financing:

- Lock interest rates early on adjustable-rate mortgages when possible.

- Establish clear fund control procedures with your lender's payment schedule.

- Verify utility grid capacity before signing construction contracts.

- Work with permit expeditors familiar with building permissions.

Professional feasibility studies are another bonus; they catch expensive surprises before you commit capital, helping you understand borrowing costs and alternative financing options that align with your equity position and timeline.

Legalization and ROI Calculations

Assembly Bill 2533 prohibits local agencies from denying permits to legalize existing ADUs built before January 1, 2020. Lenders won't include unpermitted square footage in appraisals for HELOCs or refinancing, but using the AB 2533 path to bring your unit up to code significantly increases your property's future appraised value.

This legalization process can unlock tens of thousands in borrowing capacity. Retroactive building permits bring unpermitted work into compliance, helping you access equity that vetted lenders previously didn’t recognize.

When calculating your ADU ROI, keep in mind that most San Diego ADUs break even in 7-12 years, depending on rent levels and financing structure. Studio ADUs rent for $1,900-$2,400 monthly, one-bedroom units for $2,300-$2,900, and two-bedroom units for $2,800-$3,500 in 2026.

Most San Diego ADUs break even in 7-12 years, depending on rent levels and financing structure. Studio ADUs rent for $1,900-$2,400 monthly, one-bedroom units for $2,300-$2,900, and two-bedroom units for $2,800-$3,500 in 2026.

A well-designed ADU can add $200,000-$500,000+ in property value, especially in central San Diego neighborhoods. Income verification requirements for most loan programs assume you'll generate rental income, which strengthens your debt service coverage ratio and improves your loan options.

From Planning to Move-In: Your ADU Starts with a Strategy

Can you finance an ADU in San Diego? Absolutely. The 2026 landscape offers more loan programs and municipal incentives than ever before. To find success, you’ll need to understand which financing options align with your equity position and timeline.

Streamline Design & Permitting prepares your drawings, handles permitting requirements, and sets up your project for smooth construction. We’re here to bring your project to life faster. If you're ready to move forward with your accessory dwelling unit project, reach out today for professional guidance that helps you start planning confidently.